According to the latest data from Italia Solare (based on Terna's Gaudì system), Italy's energy storage market reached a major milestone in the first quarter of 2026:

Data updated as of March 31, 2026. Source: Gaudi data.

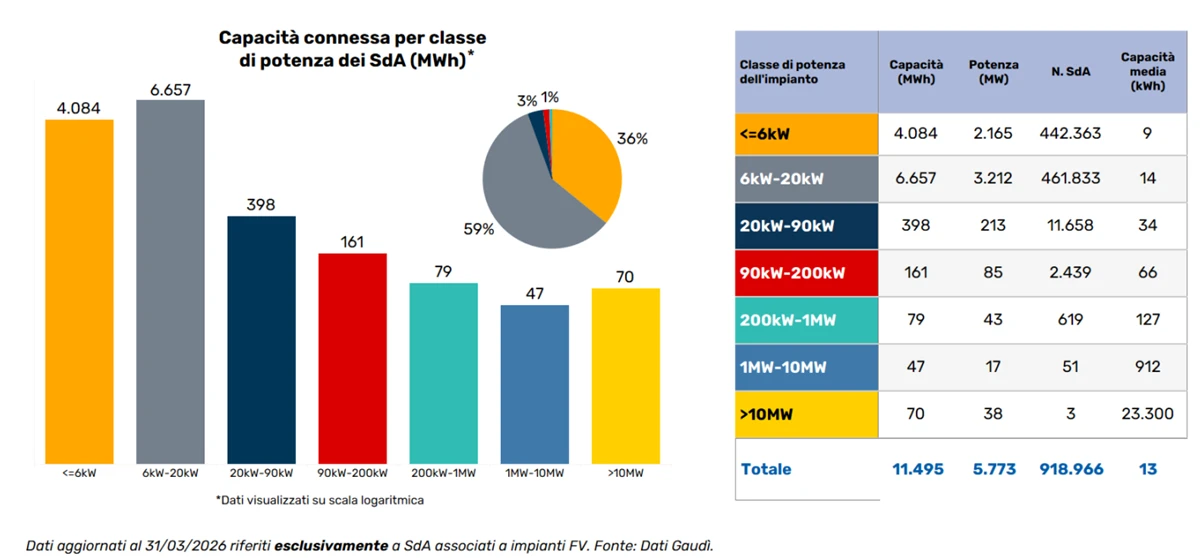

From a cumulative perspective, PV-coupled storage capacity has surpassed 11.4 GWh, accounting for 60.64% of all installations. This confirms the growing trend of integrated distributed PV-and-storage systems.

This segment consists primarily of small-capacity installations:

Most of these units were commissioned in previous years. While they significantly reduce electricity costs for owners, their potential value within power system dispatch and grid balancing mechanisms has yet to be fully realized.

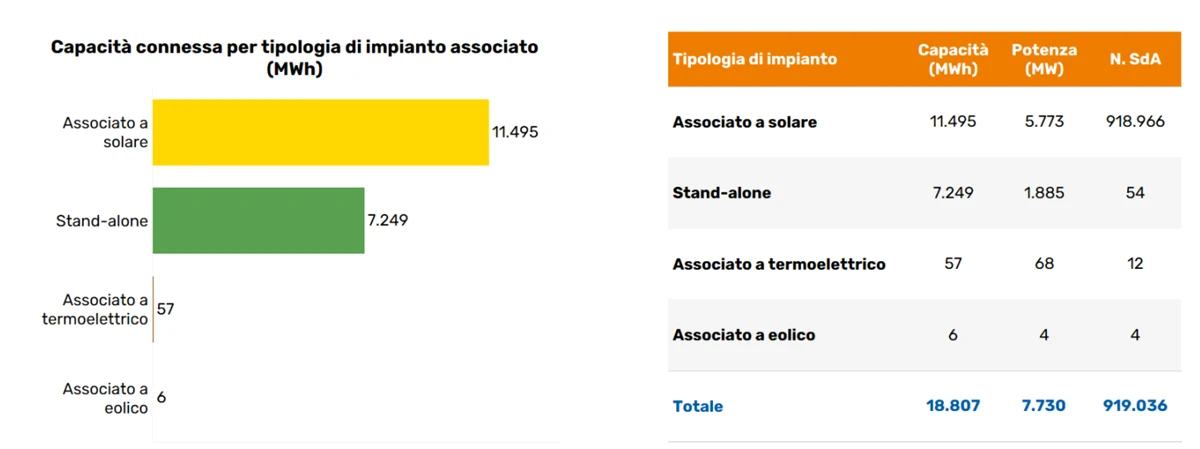

New grid-connected energy storage capacity reached 802 MWh in the first quarter of this year. Broken down by project type:

In the first quarter of 2026, the grid-connected scale of PV-coupled storage saw a decline compared to the previous quarter: capacity (MWh) fell by 9%, power rating (MW) dropped by 22%, and the number of systems decreased by 1%.

Driven by policy subsidies over the past few years, residential storage experienced rapid growth. Today, that growth is slowing significantly. Consequently, the importance of Utility-Scale (Front-of-the-Meter) and Standalone storage is becoming increasingly prominent. These systems are now the critical backbone for ensuring power system flexibility, supply security, and the integration of renewable energy into the grid.

The Italian power market is currently shifting its policy and financial incentives toward large-scale storage that can participate directly in grid balancing:

Utility-Scale Storage: Receives preferential treatment through the Capacity Market and the MACSE (Electricity Storage Forward Market), which reward systems for providing grid stability and dispatchable capacity.

Residential & C&I Storage: Revenue still relies primarily on self-consumption savings (offsetting electricity bills) and specific peak-shaving incentives. Participation in local grid flexibility projects remains largely in the pilot stage.

In terms of geographical distribution, the northern regions continue to hold a commanding lead. PV-coupled storage remains concentrated in the major regions of Northern Italy. In the first quarter:

Regarding the number of new grid-connected systems, Lombardy secured the top spot with over 5,000 new installations in Q1, with Veneto and Emilia-Romagna following in second and third place, respectively.

Italy’s energy storage target for 2030 is approximately 71.5 GWh. The vast majority of this—57.5 GWh—is designated for Utility-Scale (Front-of-the-Meter) storage. This capacity will be deployed and managed through the MACSE (Electricity Storage Forward Market) and the Capacity Market mechanisms.

To reach this ambitious goal, the market must maintain a steady and consistent growth trajectory.